[Commentary on SMM Steel Import and Export Data] Steel exports in April surged past 10 million mt again! Is May really going to witness a 'Waterloo' for steel exports?

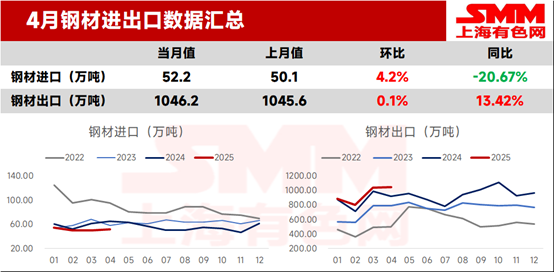

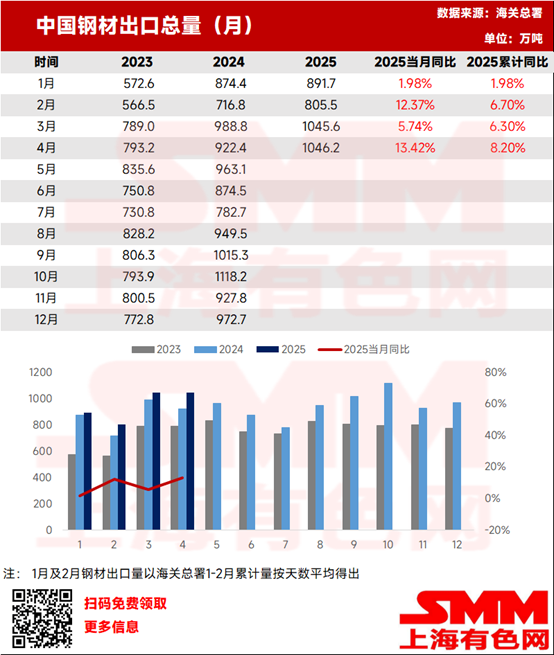

Data from the General Administration of Customs on May 9 showed that China exported 10.462 million mt of steel in April 2025, an increase of 6,000 mt MoM, up 0.1% MoM. From January to April, cumulative steel exports reached 37.891 million mt, up 8.2% YoY.

In April, China imported 522,000 mt of steel, an increase of 21,000 mt MoM, up 4.2% MoM. From January to April, cumulative steel imports stood at 2.072 million mt, down 13.9% YoY.

Overview of Steel Import and Export Data in April

- China's Steel Exports Surpass 10 Million mt in April

In April, China's total steel exports increased by 0.1% MoM, still surpassing 10 million mt, but the growth rate slowed significantly. On April 9, US President Trump suddenly announced a 90-day suspension of new tariffs on over 70 countries and regions excluding China, while only raising tariffs on China to a historic 125% (later corrected to 145%). Therefore, the increase in April exports was more pronounced during the 90-day exemption period for the US, as Chinese export enterprises were "rushing to re-export". Additionally, market rumors at the time suggested that starting from May 1, relevant tax payment certificates would be required for export customs declarations, and the phenomenon of domestic buyers rushing to export remained prominent, keeping the total export volume high.

Meanwhile, enterprises actively expanded export varieties and countries to cope with tariff pressures. For example, due to the relatively small impact of tariffs on billet exports, export volume surged 353% YoY in Q1, becoming the main force in offsetting the decline in HRC exports. Market participants were also actively expanding export trade countries, such as Saudi Arabia, Pakistan, and other Middle Eastern regions with lower export restrictions on Chinese steel, to meet their export demands. According to an SMM survey of steel mills and traders engaged in export trade in April-May, their export orders were not entirely impacted. Although HRC orders were weak, orders for billets and some cold-rolled products filled the export gap. Therefore, the total export volume remained high. However, some traders also actively seized the export market by lowering prices, which can be observed as, although the total steel export volume remained high, the average price showed a downward trend.

- China's Steel Imports Remained Low in April

In terms of imports, China imported 522,000 mt of steel in April, down 20.67% YoY, maintaining an overall net export situation. In the first four months, China's cumulative steel exports reached 37.891 million mt.

- Short-Term Outlook for Steel Exports

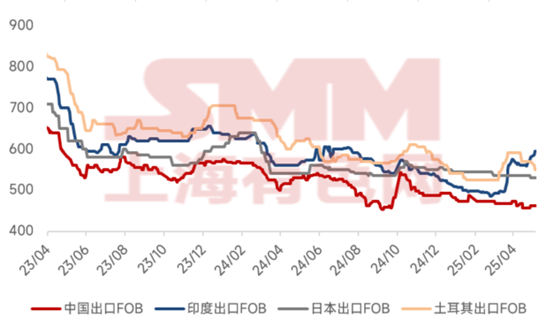

According to SMM data, as of May 8, 2025, the export offers (FOB) for HRC from India, Turkey, and Japan were $595/mt, $550/mt, and $530/mt, respectively, while China's export offer for HRC was only $462/mt. Currently, China's HRC export offer is $133/mt, $88/mt, and $68/mt lower than those of other countries, respectively.

According to the China Federation of Logistics and Purchasing (CFLP), China's manufacturing PMI stood at 49% in April 2025, down 1.5 percentage points MoM. The global manufacturing recovery momentum weakened slightly compared to the previous month. Based on China's manufacturing PMI data, the new export orders index for China's manufacturing sector was 44.7% in April, down 4.3 percentage points MoM, reflecting a gradual pullback in China's current overseas order-taking situation.

Data monitored by the World Steel Association (WSA) showed that the global crude steel production of 69 countries/regions included in the WSA's statistics was 166.1 million mt in March 2025, up 2.9% YoY. China's crude steel production was 92.84 million mt, up 4.6% YoY.

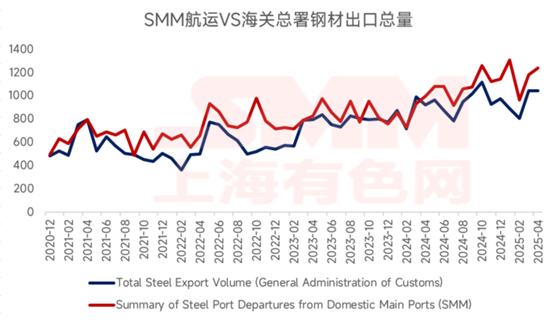

According to SMM shipping data, as of April 30, the total port departures from China's main ports in April were 12.4161 million mt, up 5% MoM, aligning with the trend of the General Administration of Customs. Considering the significant increase in billet exports in April, the growth rate exceeded the data from the General Administration of Customs! The export performance in April remained excellent. So, will exports turn worse in May as previously expected? In fact, as mentioned above, we can still cope by exporting other varieties or expanding into other overseas markets. Therefore, the overall export situation is not as pessimistic as expected. Although China's overseas order-taking situation pulled back MoM in April, this was more pronounced in the first half of the month. In the second half of April, domestic futures opened higher, stimulating overseas demand, and export order-taking improved again. According to SMM, major steel mills and export traders have basically filled their May shipment schedules and are actively pursuing June orders. Moreover, the crackdown on fraudulent purchases seems to have eased. Therefore, SMM expects steel exports to remain at a high level in May but will drop back slightly overall, with the impact more pronounced in Q3.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)